Royalty and Streaming Companies in the Precious Metals Sector: The Capital-Light Business Model Reshaping Mining Finance

In an industry defined by geological uncertainty, long lead times, and cost inflation, royalty and streaming companies occupy a distinctive, and increasingly influential, position. They are not mine operators. Instead, they provide upfront capital to miners in exchange for a contractual share of revenue or production from specific assets. The result is a business model designed to capture commodity upside and exploration optionality while largely sidestepping many of the operational headaches that burden traditional producers. For corporate audiences, whether on the operator, investor, or lending side, royalty companies are worth understanding not as a niche financial engineering tool, but as a durable source of project funding and a sophisticated way to gain exposure to mineral end-markets.

I. What “royalty” and “streaming” actually mean

Royalty and streaming agreements come in several forms, but the central idea is consistent: the investor funds a mining company today and receives a predefined economic interest linked to future production.

1) Royalty vs streaming: the practical difference:

Canadian securities guidance explicitly groups a wide set of structures under “royalty or similar interest,” including gross overriding royalties, net smelter returns, net profit interests, product tonnage royalties, and even revenue/commodity streams (e.g., rights to purchase commodities produced).

In practice, two structures dominate the listed specialist market:

1) Net Smelter Return (NSR) royalty

An NSR royalty is typically calculated as a percentage of gross revenue from a resource extraction operation, net of certain downstream costs such as transportation, refining, and smelting. A Royal Gold SEC filing (10-K glossary) describes an NSR as “a defined percentage of the gross revenue… less a proportionate share of incidental transportation, insurance, refining and smelting costs.” NSRs are popular because they are comparatively simple to administer and generally sit “high” in the economic waterfall: they are paid based on sales revenue rather than profits.

2) Streaming agreement

Streaming differs from royalties in that the streaming company typically purchases a percentage of future metal production for an upfront payment plus an ongoing “delivery payment” per ounce/unit, usually set below spot prices. The streamer then sells the metal at prevailing market prices (if no hedging in place) and captures the margin.

This structure is often used to monetize by-product metals (for example, gold and silver produced at copper mines) in a way that can be attractive to both parties.

2) Pierre Lassonde

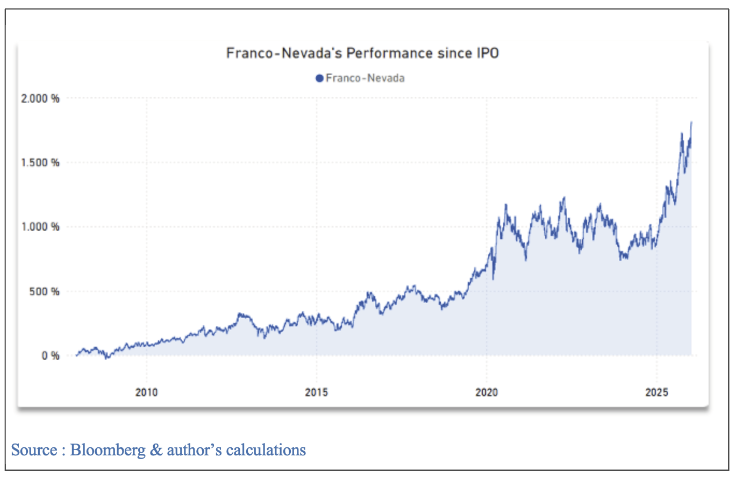

No discussion of the modern royalty/streaming model is complete without Pierre Lassonde. As cofounder (with Seymour Schulich) of the original Franco-Nevada, Lassonde helped pioneer the idea that investors could earn durable exposure to precious metals by owning contractual interests in production rather than operating mines, a structure that later became the blueprint for the listed royalty/ streaming sector. After Newmont’s 2002 combination that brought Franco-Nevada into Newmont’s orbit, Lassonde joined Newmont’s leadership and served as President in the 2000s, deepening the industry’s comfort with royalties as an institutional form of mine financing rather than “alternative capital.”

Crucially, he also played a central role in bringing Franco-Nevada to public markets in the late 2000s, an episode that reinforced the model’s credibility with investors and set the stage for royalty companies to become core allocators of mining capital across cycles.

To illustrate the powerful returns generated by Pierre Lassonde & co at Franco-Nevada, here is the performance of the share since the IPO in December 2007. That share issue enabled the company to purchased the royalty portfolio of Newmont Mining (3rd biggest gold producer at the time and on top of the podium today) for $1.2 Billion. In hindsight, that proved to be a great deal to say the least:

II. Why operators use royalty and stream financing

From a miner’s perspective, royalties and streams are neither “free money” nor a last resort. They are a strategic financing choice, particularly when management wants to:

• Avoid equity dilution (especially at cyclical lows)

• Reduce debt burden or preserve covenantheadroom

• Fund capex, expansions, M&A, or exploration without adding fixed repayment obligations

• Monetize non-core or by-product value embedded in a portfolio

Franco-Nevada explicitly positions royalty/stream capital as “low-cost and flexible funding,” helping operators avoid “excessive equity dilution” and reduce the fixed burden of debt, especially during new mine builds.

In short: royalties convert a slice of future project economics into immediate liquidity, often with fewer balance-sheet constraints than conventional debt and less dilution than equity.

III. Why investors like the model

Royalty companies have built an attractive business model around three structural advantages:

1) Operational leverage without operational responsibility

Royalty firms do not operate mines, build projects, or run exploration programs; they own a portfolio of contractual interests. This allows a lean overhead structure and reduces direct exposure to site-level execution risk. (It does not eliminate asset risk, but it changes its nature.)

2) Built-in “optionality”

A royalty on a mineral property can benefit from mine life extensions, throughput expansions, improved recoveries, and exploration success, often without requiring incremental capital from the royalty holder. Franco-Nevada highlights this “exploration optionality,” alongside limiting exposure to cost inflation.

3) Cost predictability (especially for streaming)

Streamers typically lock in a fixed delivery payment per ounce/unit. Wheaton Precious Metals (another major company of the sector) explains that this cost predictability provides direct leverage to metal prices and reduces the impact of mining cost inflation that can compress producer margins.

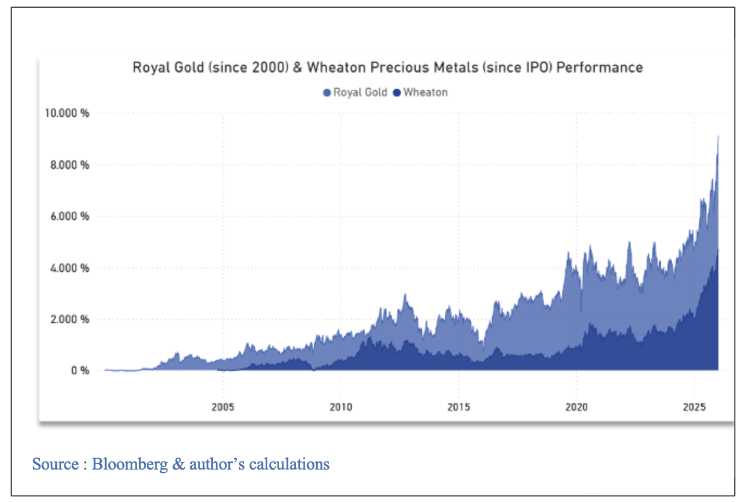

In order to illustrate the attractiveness of such business model, let’s look at the performance of the other two major royalty and streaming companies (focused on precious metals) that with FrancoNevada form the Big 3 of this sector: Wheaton Precious Metals and Royal Gold.

IV. The underwriting lens: what separates great royalty portfolios from mediocre ones

Not all royalties are created equal. The strongest franchises are built through disciplined underwriting and portfolio construction. Key diligence pillars typically include:

1) Asset quality and mine plan realism

• Reserve/resource confidence, metallurgy, infrastructure, and capex intensity

• Permitting path and execution complexity

• Expansion potential and exploration upsid (the “free upside” royalty holders want)

2) Operator strength and alignment

A royalty is only as durable as the mine’s ability to operate responsibly and economically through cycles. Counterparty capability matters for project delivery, sustaining capital discipline, and safety/ environmental performance.

3) Jurisdictional and legal enforceability

Royalties are legal claims on project economics. Jurisdiction influences not only tax and permitting stability, but also how confidently investors can rely on contract enforceability.

4) Structure and “economic gravity”

NSRs typically provide cleaner exposure to revenue, while net profit interests (NPIs) are more sensitive to cost accounting, capital recovery, and operator decisions.

V. How returns are created: a simple mental model

Royalty and streaming companies generally compound value through a combination of:

• Portfolio cash flow from producing assets

• Pipeline conversion (development assets moving into production)

• Organic growth (mine expansions and exploration adding ounces/tonnes under an existing royalty)

• New deals funded via cash flow, debt, equity, and (in some cases) asset sales/rotation

The subtlety is that the most valuable growth often comes from #3, expansions and discovery, because it can be accretive without incremental capital from the royalty holder.

A savvy investor should acknowledge that royalties are not a free lunch. They shift risk rather than eliminating it:

• Volume and grade risk: If a mine underperforms, royalties underperform.

• Commodity price exposure: The model is leveraged to prices; hedging decisions are typically limited compared with producers. An investor looking to profit from a rising gold price but afraid to take on the risk of a mining business can buy shares of a gold royalty company.

• Counterparty risk: Operator distress can delay development, curtail sustaining capex, or lead to restructuring.

• Contractual complexity: Definitions (payable metal, allowable deductions, byproduct treatment) matter, particularly for NSR calculations.

• Political/ESG risk: Permitting friction, community opposition, and regulatory change can impair project timelines. Streaming diligence explicitly flags ESG and social license as core review areas. The best illustration is the recent and ongoing situation at Franco-Nevada’s biggest asset which is Cobre Panama (one of the world’s largest copper mine) : in 2023, The Panamamian government ordered the mine to enter “Preservation and Safe Management” (P&SM), effectively halting production. Franco-Nevada registered a $1.17 billion impairment charge, writing the asset’s value down to zero. This asset represented around 15-18% of its annual revenue! In early 2026, negotiations for a potential restart are still ongoing. However, it is important to point out that the company is still extremely profitable (and zero debt!) with an operating cash flow yield above 80% for the last twelve months. The rising gold price being very helpul of course along with a diversified portfolio of royalty and streaming assets that protected the business.

VI. Bottom line

Royalty and streaming companies have created a scalable, capital-light way to participate in mining value creation. For operators, royalties can be a pragmatic funding tool, especially when the alternative is expensive equity or restrictive debt. For investors, the model offers a differentiated risk profile: direct exposure to commodity prices and exploration upside, with reduced exposure to operating cost inflation and day-to-day execution.

The most sophisticated view is to treat royalty companies not as “miners without mines,” but as specialist capital allocators underwriting complex, long-dated claims on real assets, where structure, counterparties, and optionality determine outcomes.

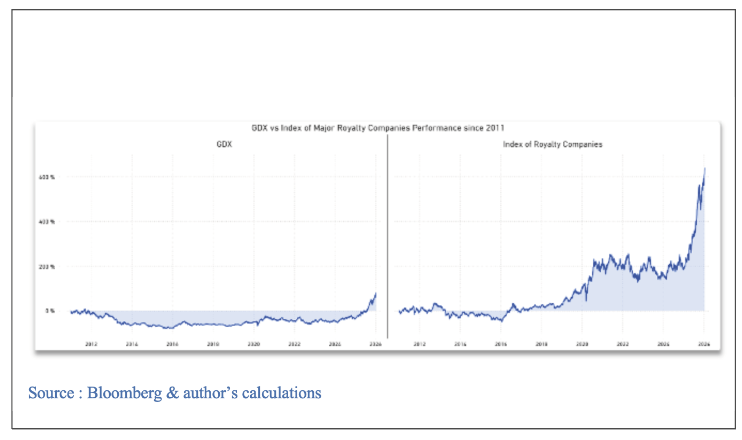

To conclude, let’s illustrate in two ways the superiority of the described business model:

Comparing the performance of an index of royalty companies composed of 8 companies (the biggest ones) versus the performance of the GDX, the well-known gold miner’s index. We elected to start the calculations in 2011, the year where the last major gold and silver bull market peaked, that way we point out how precious metals royalty businesses can outperform producers even with gold prices not performing. Notice how the GDX only started to be positive lately thanks to the outstanding gold price moves. The inflationary effect on operational expenditures were detrimental to miners but Royalty & Streaming companies were shielded from such issue and outperformed.

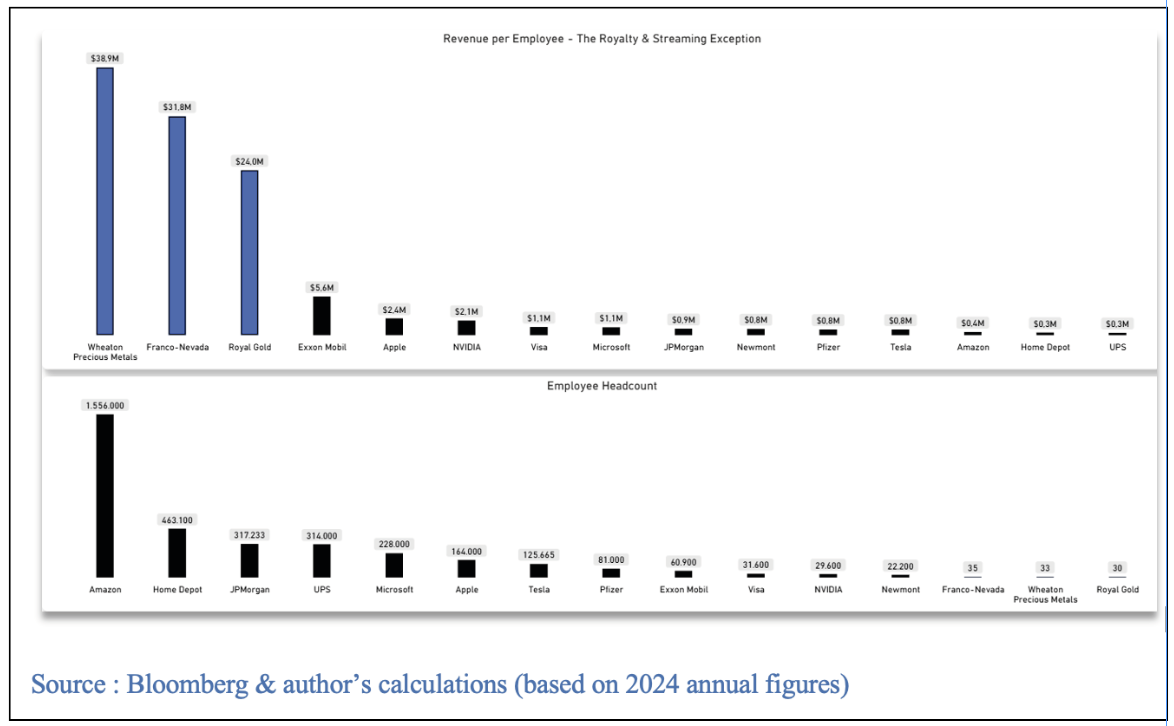

Another bright side of these companies: the socalled operational leverage. Royalty companies rank second to none in the revenue per employee metrics. A small team of competent people can produce outsized amounts of revenue. Hence, the majors of the sector usually show a 60-80% operating cash flow yield which would make the profitable software companies (usually very high margin businesses) quite envious!

The below illustration displays the revenue per employee of the big three royalty companies compared to some blue chips US companies: