Prepayment financing: a mutually beneficial arrangement… Under certain conditions!

Mining is a unique industry in many ways. For one thing, it is highly capital intensive, requiring heavy investment and a significant amount of cash to operate on a daily basis. It also entails a set very distinct operating cycles, each phase of which has its own specific economic and financial challenges. Upstream, juniors must explore and study the potential of a mine without any guarantee of future production flows. This is the time for IPOs and successive capital increases, as the outline of the projects comes into focus. In contrast, the mass production and industrialisation phase occur when the mines are mature, the flows are known, and the infrastructure needed has been financed. At this stage, producers are able to provide banks with the necessary guarantees to obtain credit. The nature of the financing is logically consistent with this pattern: the more structured and developed the mining project is, the better the visibility of its future revenue streams and the less dilutive the financing.

There remains an intermediate phase between these two extremes, during which the exploration risks and technical hazards are sufficiently controlled to dispense with risk redistribution (and thus avoid dilution), but still too high to offer banks the many guarantees they require. This is the period of infrastructure deployment and production launch. So-called ‘alternative’ private financing makes it possible to address this critical phase. These come in several flavours. However, while these several possibilities may all be available to mining companies, they are by no means equal. Above all, they do not all offer a mining company the same peace of mind, far from it.

Royalty financing offers the mining company financing in exchange for a proportion of the turnover or operating profit to be generated by the mining project in the future. While the financial charges are adjustable and the balance sheet remains undiluted, the company’s liability continues throughout the life of the mine. Moreover, such a mechanism makes it impossible to determine the cost of capital ex ante; financing costs can be estimated only with great difficulty and after the fact. The same constraints apply to streaming, which permanently earmarks for the creditor a predefined portion of a mine’s future production, at a price well below market rates, in return for the initial financing.

Royalty financing offers the mining company financing in exchange for a proportion of the turnover or operating profit to be generated by the mining project in the future. While the financial charges are adjustable and the balance sheet remains undiluted, the company’s liability continues throughout the life of the mine. Moreover, such a mechanism makes it impossible to determine the cost of capital ex ante; financing costs can be estimated only with great difficulty and after the fact. The same constraints apply to streaming, which permanently earmarks for the creditor a predefined portion of a mine’s future production, at a price well below market rates, in return for the initial financing.

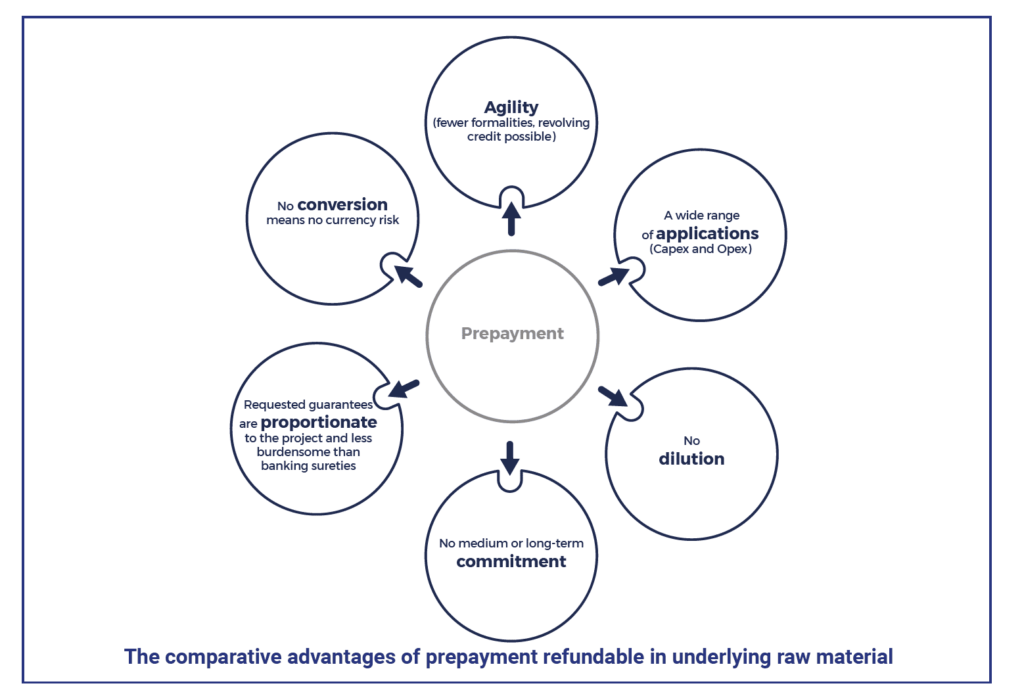

To these perpetual burdens, there exists an alternative: prepayment. The creditor typically advances funds in exchange for later repayment in commodity produced by the mine. There are two possible scenarios. Either the repayment is made in the form of deliveries of commodity, whose quantity is calculated according to a fixed amount of currency (generally US dollars), or as regular deliveries of a fixed quantity of the underlying commodity of the project. For the mining company, the differences between these two options are critical.

Let us assume that the raw materials prices depreciate between the time the financing is granted and when it is actually repaid. According to the first arrangement, the mining company must produce more to repay its financing. The capture of an increasing share of production in turn weakens the economic equation of the mining company and hampers its ability to finance its development. In extreme cases, as in the event of default, guarantees are called, and the operator may lose all its assets to its creditor. This risk is far from theoretical, as dramatic examples from the past attest.

By definition, a repayment comprising the delivery of a predefined and fixed volume of commodity protects the mining company from this risk. Depreciation in the price of the underlying material has no impact on the quantity to be delivered to its creditor, which in this case is both the operator’s financier and its first buyer. It is the creditor, and no one else, who bears the risk of a fall in the price of the commodity. At most, the mining company assumes an opportunity cost if the price goes up. But at no point, whatever the price trend, is its survival or control of its assets at stake, provided of course, that it respects the schedule agreed to with its creditor.

On the express condition that it be repaid in the form of a predefined and fixed volume of commodity, prepayment financing offers further advantages. The repayment schedule is staggered according to production forecasts, allowing the operator to secure their cash flows and therefore the ability to continue operating. In addition to being non-dilutive, it is also less burdensome to set up and less intrusive. Designed with a short lifespan, it does not commit the parties beyond the transaction. Once the initial audits have been carried out and following a successful initial prepayment, new tranches can be set up easily as desired, taking into account the realities of production and the updated price of underlying raw materials. This is a way for the mining company to ensure that its financing is truly in line with its current economic situation. Unlike a predatory agreement, this type of financing gives the mining company a great deal of leeway to control its balance sheet and concentrate on its core business: extraction and processing. This is a key advantage for mining projects in their critical development and production start-up phase.

It is this form of non-predatory prepayment financing that the OCIM Group offers to a growing group of mining operators around the world, supporting their development in a mutually beneficial and virtuous cycle.